All about SGST, CGST, IGST and UTGST

Implementation of GST in India was a big move, as it marked a significant indirect tax reform in the country. The amalgamation of a large number of taxes which was levied at a central and state level into a single tax had expected to have big advantages. Almost about four years ago, GST had replaced 17 local levies like excise duty, service tax, VAT and 13 cesses.

Most of the complex indirect system problems

have also been eased by GST with a simple, transparent and technology-driven

tax regime and has thus integrated India into a single common market. Further,

Tax arbitrage across states that distorted business investment decisions has

also been eliminated by the implementation of GST. In this article, we’ll talk

about the different types of GST namely SGST, CGST, UTGST and IGST, their

structure and a basic difference between them.

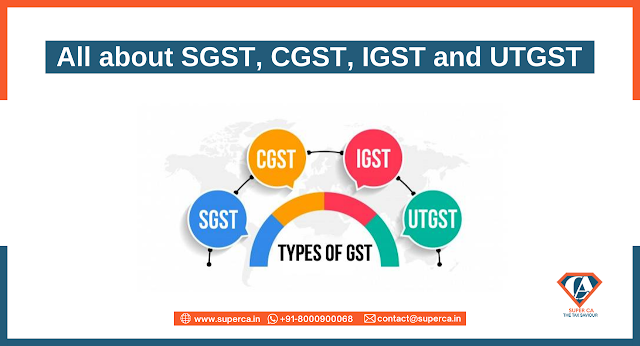

Types of GST and its Explanation

As per the newly implemented GST regime, there are 4 different types of GST namely :

Integrated Goods and Services Tax (IGST)

State Goods and Services Tax (SGST)

Central Goods and Services Tax (CGST)

Union Territory Goods and Services Tax (UTGST)

As per the law, the central government will collect CGST, SGST or IGST depending upon whether the transaction is intrastate or interstate. When the supply of goods or services happens within a state called intra-state transactions, then both the CGST and SGST will be collected. Whereas if the supply of goods or services happens between the states called inter-state transactions, then only IGST will be collected.

Central Goods and Services Tax (CGST)

CGST expands to the Central Goods and Services Tax and is charged on the intrastate supply of goods and services by the central government and is governed by the CGST Act.

The CGST is collected along with SGST. Both the Central and State governments collect the taxes and combine their levies with an appropriation proportion between them. Further, as per the Goods and Service Tax Act, the taxes which are imposed on all the intra supplies of goods and services and it shall not be more than 14% each.

State Goods and Services Tax (SGST)

As we discussed above on intra-state supply CGST will also be applicable but CGST will be controlled by the Central Government. SGST expands to State Goods and Services Tax. It is the tax imposed on Intra-state supplies of goods and services which is collected by the State Government and will be governed by the SGST Act. If there is any tax liability under SGST then it can be set off in opposition to SGST or IGST ITC only.

Union Territory Goods and Services Tax (UTGST)

The Union Territory Goods and Services Tax or UTGST is the equivalent to SGST which is levied on the supply of goods/services in the Union Territories (UTs) of India. The UTGST is applicable on the supply of goods and/or services in Union Territories like Andaman and Nicobar Islands, Chandigarh, Daman Diu, Dadra, Nagar Haveli, and Lakshadweep.

The UTGST is governed by the UTGST Act and the revenue earned is collected by the Union Territory government. The UTGST can be seen as a replacement for the SGST in Union Territories, but the concept of CGST will be the same.

Integrated Goods and Services Tax (IGST)

Integrated Goods and Services Tax or IGST is levied on all inter-state supplies of goods and services. It is also applicable on the imports and exports of goods and services, and on supplying activities related to SEZs or Special Economic Zones. In the case of interstate tax collection, instead of separately charging taxes for the Center and the State, the Government collects a single IGST, which is later divided equally.

In IGST, the exports are zero-rated and the tax is shared between the central and state government.

Now let's take an example and understand the practical implications of these

Let’s say, a dealer in Bihar is selling goods to the consumer in Bihar worth Rs. 10,000. The GST rate is 12% consisting of 6% CGST and 6% SGST, in such cases, the dealer collects Rs. 1200 and Rs. 600 will go to the central government and Rs. 600 will go to the Punjab government.

Now, if the dealer in Bihar had sold goods to a dealer in Rajasthan worth Rs. 1,00,000 with the GST rate being 12%, then in such cases the dealer has to charge Rs. 12,000 as IGST. This IGST collected will go only to the Centre

About online GST registration

As per the GST rules, it is mandatory for a business/supplier that has a turnover of above Rs.40 lakhs (Rs 10 lakhs for special category states present in hill states and North-Eastern states) to register as a normal taxable entity through online GST Registration Process. In online GST registration, no manual intervention or physical paper submissions is required. The online process is as simple as it may sound. It is usually completed within 4-6 working days and the supplier is allotted a 15-digit GSTIN (GST identification number) and a certificate of registration by the GST department. Various types of online GST Registration are described under the GST Act

If the organizations fulfilling the eligibility criteria carries on business without registering to GST, it will be an offence under GST and heavy penalties will apply.

Final Words

As a federal country, both the Center and the States are assigned the powers to levy and collect taxes. Both the Governments perform various duties, as per the Constitution, and hence they need to raise tax revenue. This type of tax structure is implemented in order to help taxpayers take the credit against each other thus safeguarding the “One Nation, One Tax” motive.

.jpg)

Comments

Post a Comment